Original research

Data & Press

Original research on home affordability across the US, Canada, and the UK — free to cite, link to, and use. Every figure below is sourced and dated. If you're a journalist, researcher, or writer working on a housing story, the data below is yours to use.

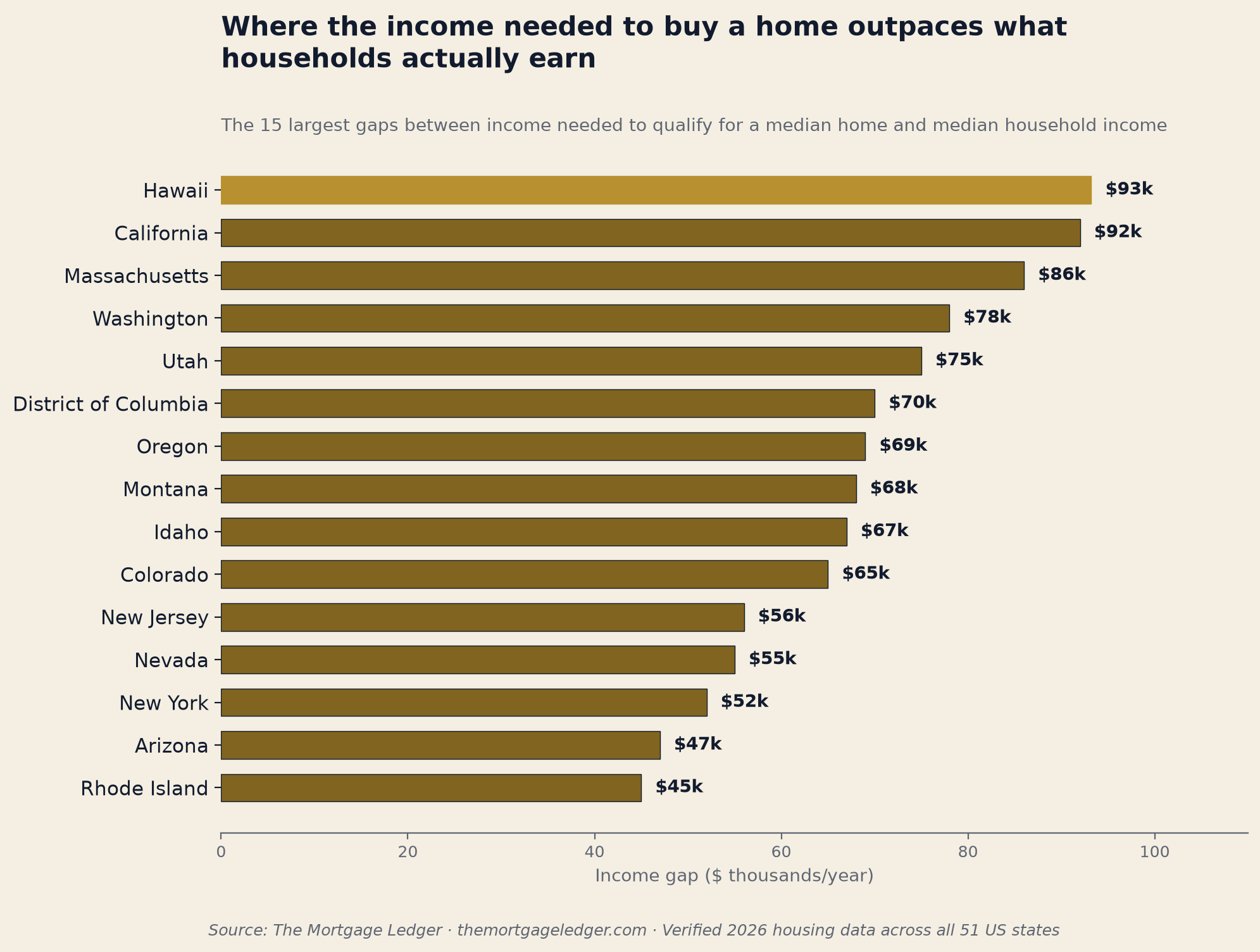

In 29 of 51 US states, a single median income is no longer enough to buy a median-priced home.

We compared the income a lender typically wants to see (using the standard 28% debt-to-income guideline) against actual median household income, in every US state. In 29 states — including California, New York, Washington, and Colorado — the gap is large enough that a single earner at the median household income can no longer comfortably qualify for a median-priced home alone.

Nationally, the median home now requires roughly $112,900/year in income to buy at standard lending guidelines, while the median household earns roughly $83,700 — a $29,200 gap.

- Hawaii — needs $93,209/year more than the median household earns

- California — needs $92,000/year more than the median household earns

- Massachusetts — needs $86,000/year more than the median household earns

Use this chart

Free to embed or republish with credit. The source caption is part of the image.

Download the chart (PNG, 2,000 px)

Embed code

<img src="https://themortgageledger.com/press/income-gap-by-state.png"

alt="The 15 largest gaps between the income needed to buy a median home and median household income, by US state"

width="1000" />

<p>Source: <a href="https://themortgageledger.com/press#dual-income-required">The Mortgage Ledger</a></p>Source: Zillow ZHVI · U.S. Census ACS · Splitero · Verified 2026-06-30

Link directly to this finding: https://themortgageledger.com/press#dual-income-required

Home insurance works fundamentally differently in the US, Canada, and the UK — and it's not just about price.

Beyond cost, the three countries handle flood coverage completely differently. In the UK, flood damage is typically included in a standard home insurance policy. In the US, flood coverage is never included — it always requires a completely separate federal (NFIP) policy. In Canada, overland flood coverage is an optional private add-on, a genuinely distinct third model that's only been widely available since 2015, and can be unavailable altogether in the highest-risk zones.

This isn't a minor technical difference — it's the kind of thing that catches homebuyers off guard when they assume their coverage works the way it did in a different country.

The full three-country comparison, including costs by state, province, and nation: Home insurance, explained.

Source: Insurance.com (US) · IBC (CA) · ABI (UK) · Verified 2026-07-01

Link directly to this finding: https://themortgageledger.com/press#insurance-by-country

The median homeowner has roughly 40 times the net worth of the median renter.

Federal Reserve data shows the median homeowner's net worth sits around $396,200, compared to roughly $10,400for the median renter. The honest caveat, worth including in any story that cites this: the gap reflects both the genuine wealth-building effect of homeownership (forced savings through equity, leverage, protection from rising rent) and the fact that wealthier households are more likely to become homeowners in the first place — it's not purely causal.

The mechanisms and caveats in full: Why real estate builds wealth — and when it doesn't.

Source: Federal Reserve Survey of Consumer Finances / Aspen Institute · Verified 2026-06-30

Link directly to this finding: https://themortgageledger.com/press#homeowner-wealth-gap

Methodology, in brief

Figures are drawn from Zillow Home Value Index data, U.S. Census Bureau American Community Survey data, and Federal Reserve Survey of Consumer Finances data, current as of our most recent verification pass (see the date on each figure). Full methodology and sourcing: Methodology & Sources.

For journalists

Have a housing story that could use fresh data? We're happy to pull a custom cut of this dataset for your specific angle — by state, by metro area where we have the data, or year-over-year. Reach us at themortgageledger@gmail.com.

All figures are educational estimates from public data — see each figure's source. Free to cite with credit to The Mortgage Ledger.